Key JOLTS indicators weaken further in June, raising recession concerns

A sharp drop in the hiring rate tops the list of concerns that arose from the latest JOLTS data, reinforcing that the key economic risk is that the US enters a recession in 2H24.

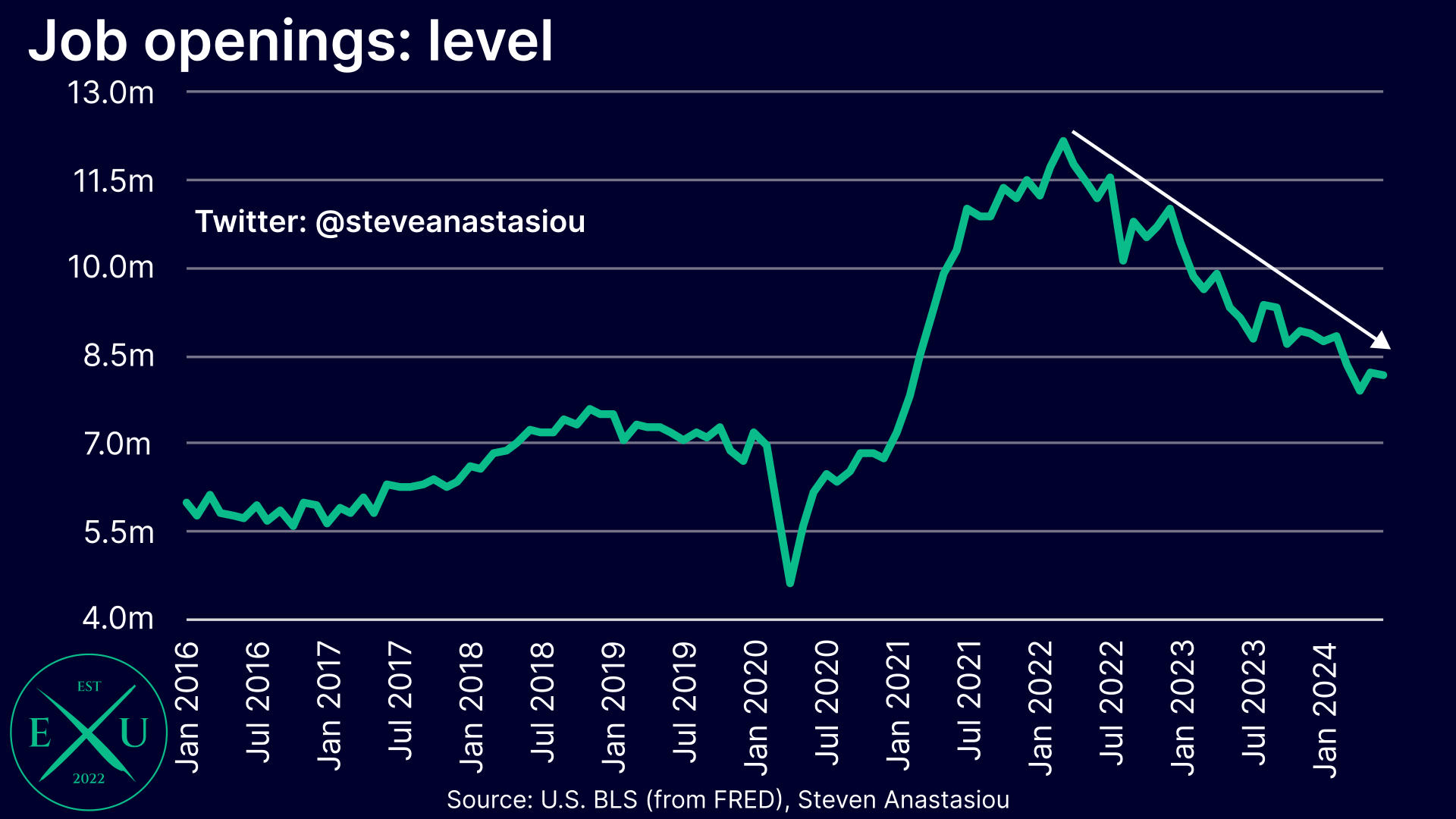

Job openings continue to fall, with private sector job openings now back to pre-COVID levels

Total nonfarm job openings fell to 8.18m in June, from 8.23m in May.

Given that the unemployment level has also been rising, the ratio of job vacancies to unemployed individuals fell to 1.20 in June, the lowest level since June 2021.

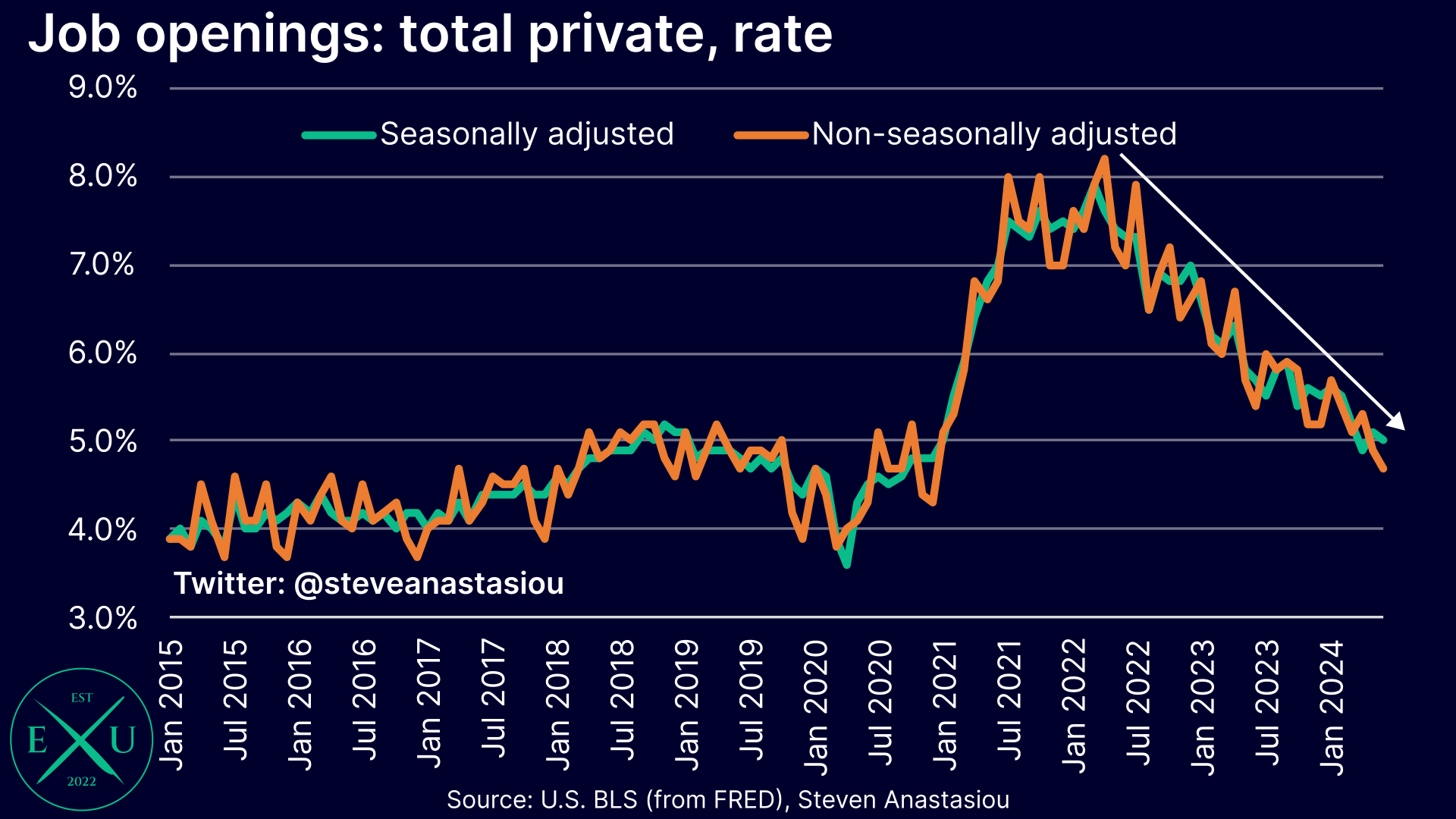

The private sector job openings rate, which is more impacted by cyclical shifts in the economy than overall nonfarm payrolls, fell to 5% in June. The fall has been softened by seasonal adjustments, with the non-seasonally adjusted private job openings rate falling to 4.7%, which is already in-line with pre-COVID levels and trending lower still.

The more timely Indeed survey of job openings, which had recorded 19 consecutive MoM declines to June, has shown signs of stabilising in July, with MoM growth up 0.67% to 26 July. Despite the MoM increase, Indeed’s job openings measure continues to point to further downside for the BLS’ measure of job openings in July.

Despite the uptick in overall job openings, Indeed’s measure of new job openings (i.e. those posted on Indeed within the last seven days) is on track for a fifth consecutive MoM decline in July, with MoM growth -1.0% to 26 July. This suggests that as opposed to a significant increase in employer demand, that the MoM increase in Indeed’s job openings index was driven by lower hiring rates, which as discussed below, is corroborated by the latest BLS data.