Latest PCE inflation data provides positive signs, but the Fed will want more before it cuts rates

While April's PCE Price Index data revealed positive signs on services prices, the Fed will likely want additional disinflationary evidence before cutting rates. I continue to expect 2H24 rate cuts.

In case you missed it, I recently released a research report covering the second revision to 1Q24 US GDP data, which painted a notably more modest economic picture and further suggested that the US may be experiencing a material economic slowdown — you can read it here. The next report to be released will cover the latest PCE income and spending data and what this tells us about the state of the US economy and its likely direction.

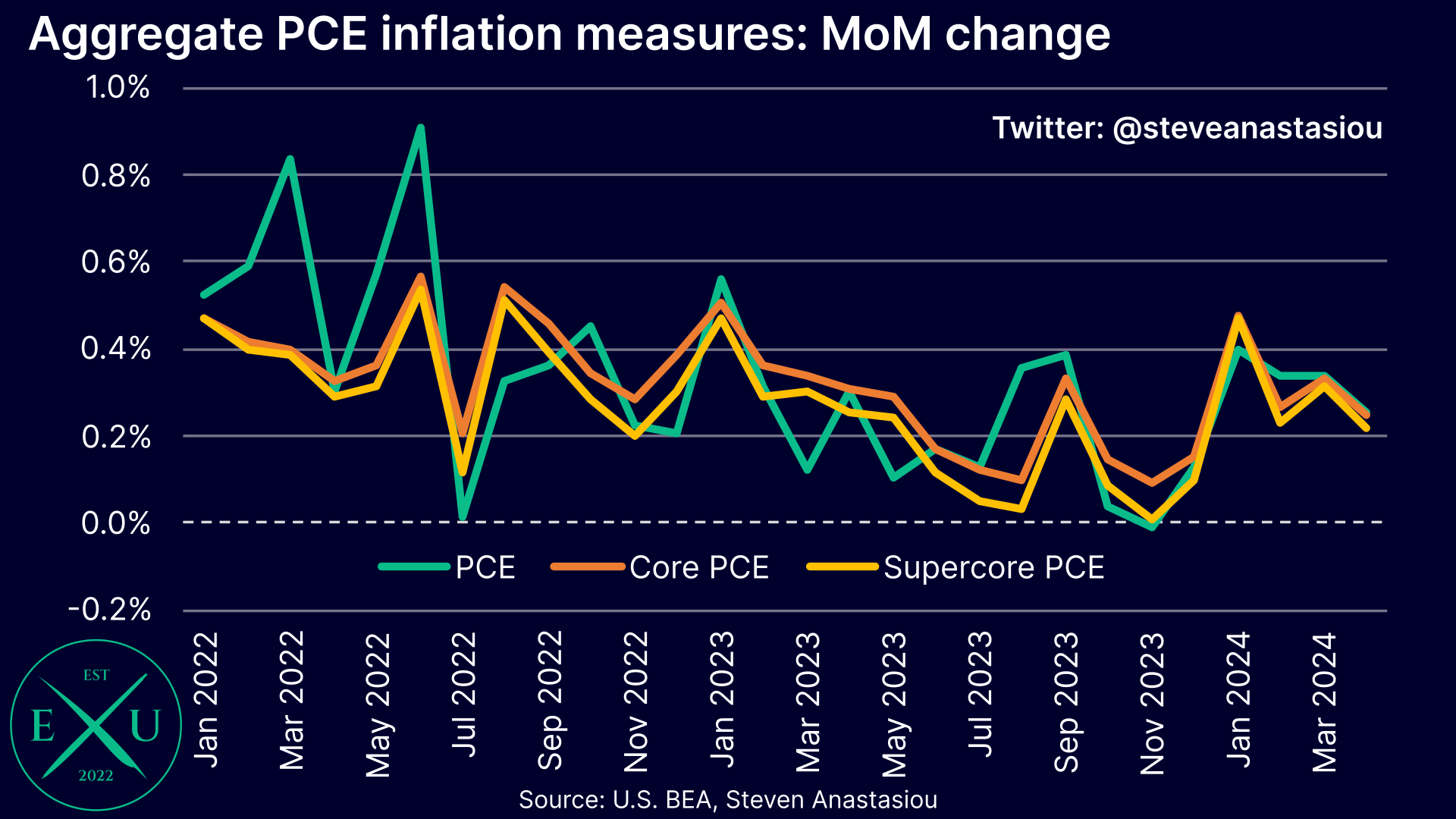

Aggregate PCE inflation measures show some MoM improvement, but YoY growth remains stuck

The headline PCE Price Index (PCEPI) rose by 0.26% MoM in April, marking the slowest pace of growth since December and the third consecutive month of disinflation, which was pleasing given that gasoline prices saw another big MoM jump (up 2.7% MoM).

The core PCEPI rose by 0.25%, which was also the slowest pace of growth since December, while the supercore PCEPI (defined here as the core PCEPI less the lagging housing services component) rose by 0.22% MoM, which again, was the slowest pace of growth since December.

Now that January’s big jump is out of the way, 3-month annualised growth dropped materially across all key aggregate measures: headline PCEPI growth fell to 3.8% (from 4.4%), core PCEPI growth fell to 3.5% (from 4.4%) and supercore PCEPI growth fell to 3.1% (from 4.1%).

6-month annualised growth continues to be impacted by January’s spike in MoM growth and the broader uptick in price growth in 2024 versus 2H23: headline PCEPI growth rose to 2.9% (from 2.5%), core PCEPI growth rose to 3.2% (from 3.0%) and supercore PCEPI growth rose to 2.7% (from 2.4%).

YoY growth continues to stabilise at around current levels, with headline PCEPI growth remaining at 2.7% (but with two-decimal place growth coming in at 2.65%, it almost rounded to 2.6%), core PCEPI growth remaining at 2.8% (but with two-decimal place growth of 2.75%, it almost rounded to 2.7%) and supercore PCEPI growth holding at 2.2% for a fifth consecutive month (but with two-decimal place growth of 2.15%, it almost rounded to 2.1%).

While the hotter price growth in 2024 versus 2H23 has raised concerns about the outlook for inflation, the relative stabilisation in YoY growth indicates that the uptick in MoM growth across the first four months of 2024 is broadly consistent with price growth seen this time last year. This potentially indicates that inflation may moderate in the second half, as it did last year — note that for a variety of reasons (including wage growth trends, spot market rents and vehicle price trends), I am currently forecasting a material moderation in monthly core US CPI growth in 2H24 (see “US CPI Medium-Term Forecast Update: Don't rule out multiple rate cuts just yet” for more detail).