US CPI Medium-Term Forecast Update

A significant step-up in inflation to begin the year has resulted in material increases to my medium-term US CPI forecasts — read on to find out how big of an impact this may have on Fed policy.

In this latest research piece, I update my medium-term US CPI forecasts (covering all of 2024), which have been revised higher on account of the spike in monthly CPI growth during the first two months of this year.

In addition to detailing these latest forecasts, I outline what key leading indicators of inflation are signalling, and the related implications for Fed policy. In addition to providing a high level overview of my forecasts across key CPI aggregates, this report also provides an in-depth breakdown of some of the key components of my CPI forecast (including durables, food, the CPI’s rent based measures, and a range of other CPI services items).

At over 2,700 words, this latest research update provides significant value for medium-term planning, and extends the comprehensive research coverage that has already been provided on inflation over the past month.

Given the significant value provided within this report, like my US CPI Preview, this report will be largely paywalled, as premium subscribers help to ensure the ongoing future and growth of Economics Uncovered.

Over the coming days, I intend to release my monthly US Jobs Report Review and US CPI Preview, adding to the 11 research reports (including this one), that have been released over the past month.

To fully benefit from this research coverage, and to help support my independent research offering, please consider becoming a paid subscriber.

CPI forecasts continue to apply a downward bias on account of the policy backdrop & leading indicators

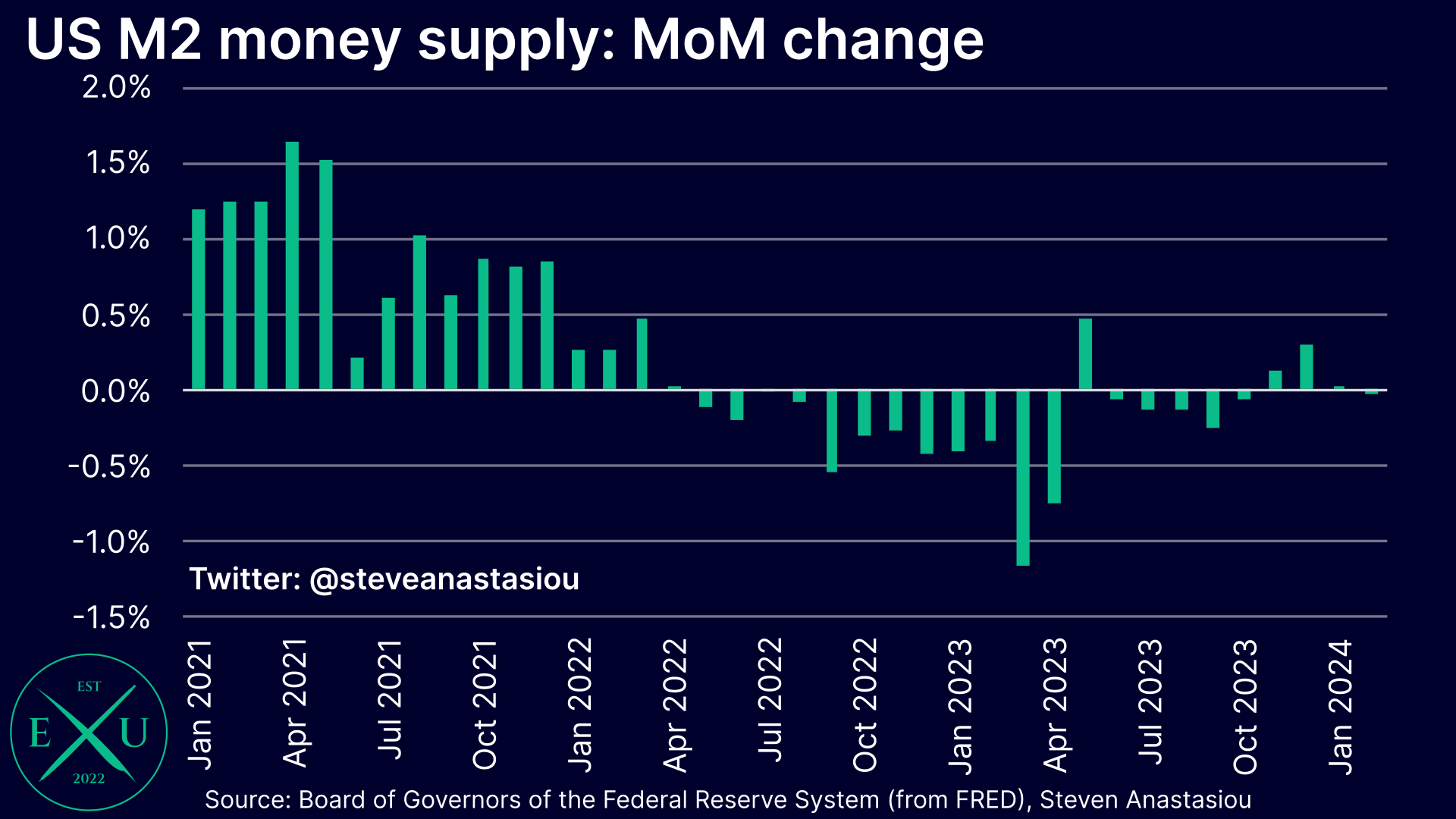

Given that the Fed’s monetary policy tightening has had the effect of constraining growth in the M2 money supply (which remains YoY negative), I continue to believe that it remains appropriate to incorporate a gradual downward bias to my medium-term US CPI forecasts.

In addition to the impact of a constrained M2 money supply, forward indicators of wage growth also point to lower services price growth as the year progresses (for in-depth detail on this topic, see “Deciphering the outlook for services prices”).

Shown below is the historical link between wage growth and core CPI services prices, as well as an extrapolation of the outlook for wage growth, that is based on a range of leading indicators. These indicators are broken down in detail within the above mentioned research piece.